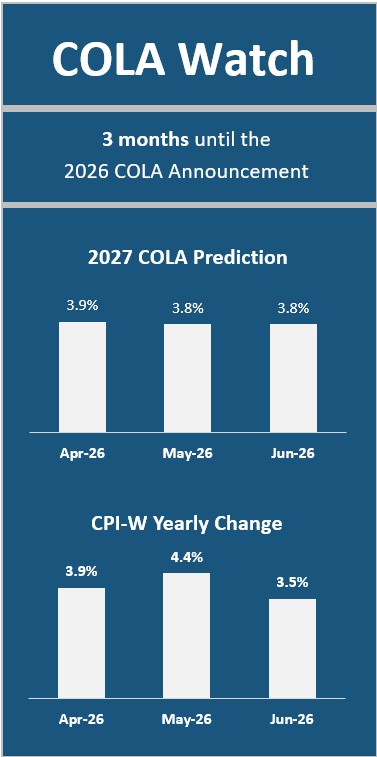

TSCL predicts that Social Security’s 2027 Cost of Living Adjustment (COLA) will be 3.8 percent, unchanged from last month and 1.0 percentage points higher than this year’s COLA of 2.8%. If TSCL’s projected 2027 COLA took effect today, average benefits would rise by $73.62, from $1,937.53 to $2,011.15.

Meanwhile, Congress reintroduced the Social Security 2100 Act, which would provide long-term relief to seniors losing buying power due to high inflation. The bill would raise benefits by 2 percent, set the new minimum benefit to 125 percent of the Federal poverty line, change the COLA calculation to the CPI for the Elderly (CPI-E), and improve the benefits calculation formula.

If passed, the bill would lengthen the program’s lifespan. The bill would increase the Social Security payroll tax and expand it to cover income over $400,000, which would shore up its trust fund for an additional 32 years.

However, passage is unlikely. The Social Security 2100 Act was first introduced in 2017. GovTrack gives the 2026 bill a 0 percent chance of passing.

Key Insights:

- The Social Security 2100 Act would fulfill many of American seniors’ wishes around improving the Social Security program. TSCL’s research has consistently shown that majorities of seniors want Congress to enact a general benefits increase and change the inflation index to calculate COLAs to one more reflective of their economic experiences.

- The single most impactful provision of the bill, at least in the short term, would be raising the minimum benefit to 125 percent of the poverty line. In 2026, the Federal poverty line for a household of one is $15,650 per year, or $1,304 per month. About one in 10 seniors, or 5.6 million people, survive on less than $1,000 per month according to our research.

- However, the bill would fall short in one key area—immediate relief. TSCL has long called on Congress to pass a one-time stimulus of $1,400 for all American seniors to make up for the long-term decay in Social Security’s buying power, and the bill does not deliver in this area. One that would, however, is the Social Security Emergency Inflation Relief Act, introduced this year, which would increase benefits by $200 a month over six months ($1,200 total).

TSCL Executive Director Shannon Benton says…

- “Although the Social Security 2100 Act is unlikely to pass in the current Congress, it should. The bill is the gold standard for Social Security reform and accomplishes the majority of changes older Americans want to see for the program.”

- “The reality is that poverty is increasing rapidly among American seniors, who make up the fastest-growing portion of the homeless population. Adjusting the minimum benefit to above the Federal poverty line would almost certainly slow this trend, although more holistic efforts may be required to stop it entirely.”

- “Right now, we have a golden opportunity to act. The 2026 Social Security Trustees Report projects that the program’s trust fund will reach insolvency in Q4 2032, forcing an automatic benefits cut. Congress will almost certainly have to pass a bill to address the program’s finances in the next few years, which provides a perfect chance to simultaneously shore up benefits for the next 100 years and continue the program’s legacy.About TSCL:

The Senior Citizens League (TSCL) is one of the nation’s largest nonpartisan seniors’ groups. Established in 1992 as a special project of The Retired Enlisted Association, our mission is to promote and assist our members and supporters, educate and alert senior citizens about their rights and freedoms as U.S. citizens, and protect and defend the benefits seniors have earned and paid for. TSCL consists of vocally active senior citizens concerned about the protection of their Social Security, Medicare, and veteran or military retiree benefits. To learn more, visit https://seniorsleague.org/about-us/.

About the TSCL COLA Model:

TSCL issues a new prediction of the next COLA for Social Security each month using our statistical model. The model incorporates the Consumer Price Index, the Federal Reserve interest rate, and the national unemployment rate to make its predictions. The model’s predictions update throughout the year, adjusting in response to economic conditions.